Why is the Chinese Economy Ailing?

China’s Economic Slowdown: From Pre-COVID to Post-Pandemic Struggles

China’s economic landscape has undergone significant changes in recent years, transitioning from a rapid growth trajectory to a period of stagnation. As the world’s second-largest economy, China’s struggles have far-reaching implications, impacting global trade and investment patterns. This article explores the factors contributing to the Chinese economy’s slowdown, examining pre-COVID trends, the pandemic’s effects, and the ongoing challenges in its recovery.

1. The Early Signs: China’s GDP Slowdown Before COVID-19

China’s economy had been showing signs of slowing down even before the COVID-19 pandemic. Historically, China maintained remarkable growth rates, averaging 10% annually, which transformed the country into the second-largest global economy. However, as early as 2018, China’s growth had begun decelerating, and there were several reasons behind this.

a) Shift from Manufacturing to Consumption:

China’s rapid economic growth was largely driven by its manufacturing sector, with China being the “world’s factory” for several decades. However, in recent years, the country has been shifting its economic model towards a more consumption-driven economy. This transition is challenging, especially given the global competitive landscape. Manufacturing jobs, which previously fueled growth, started declining, and domestic consumption growth wasn’t sufficient to fill the gap.

b) Aging Population:

China faces a demographic challenge with an ageing population and a shrinking workforce. The effects of the country’s one-child policy are now being felt, with fewer young workers entering the labour force. The population aged 60 and above is growing faster than those in the workforce, putting pressure on social services and reducing labour supply, both of which dampen economic growth. Market projections suggest that China is projected to have the sharpest spike when it comes to an ageing population.

c) Debt and Overleveraging:

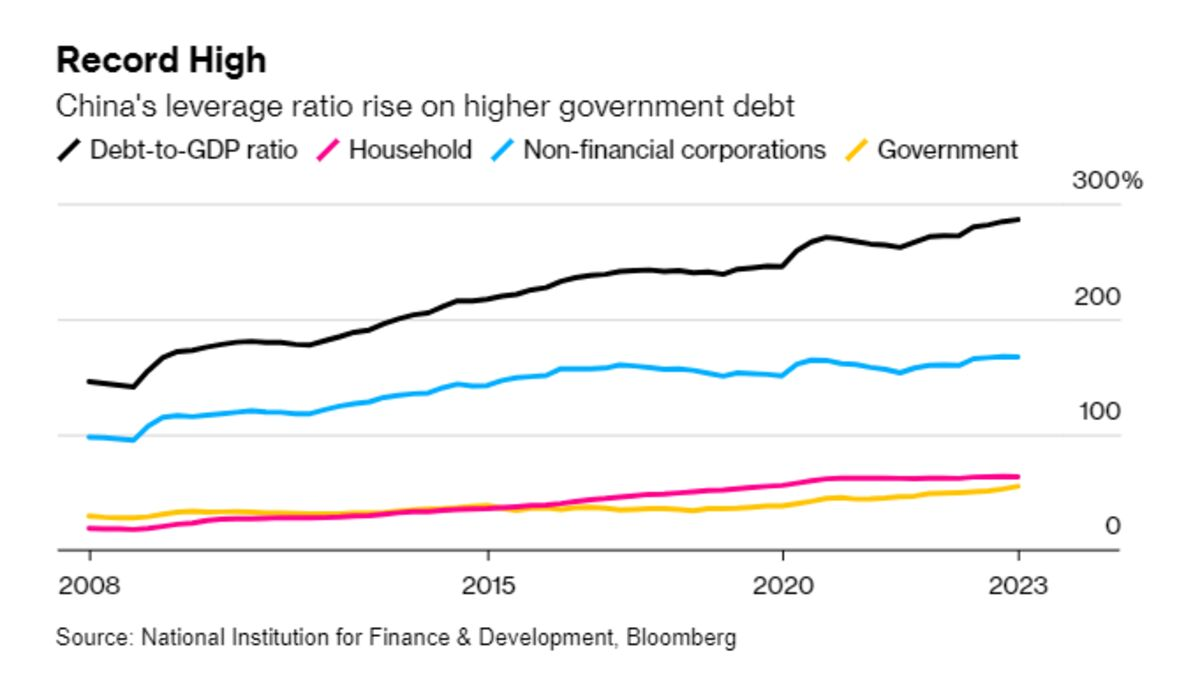

China’s growth has been fueled by large-scale infrastructure investments, often funded by debt. By 2019, local governments and state-owned enterprises were heavily indebted, leading to inefficiencies and misallocation of capital. Additionally, the country’s real estate market was overheated, with significant amounts of debt being tied to property investments, creating a bubble that economists warned was unsustainable.

For reference, the Chinese Debt to GDP ratio is at an all-time high of close to 300%,

d) Trade Tensions with the U.S.:

The U.S.-China trade war, which began in 2018 added to China’s economic challenges. Tariffs on Chinese goods disrupted trade flows and hurt Chinese exporters. The trade war also forced companies to rethink their global supply chains, causing some businesses to relocate production outside of China, reducing foreign investment and industrial activity in the country.

By 2019, China’s GDP growth had already slowed to around 6%, its weakest in nearly three decades, setting the stage for the economic turbulence that followed the onset of the COVID-19 pandemic.

2. The Effects of COVID-19 on China’s Economy

The arrival of COVID-19 in early 2020 hit China hard, both as the origin of the virus and as a globally connected economy. Strict lockdowns, business closures, and disruptions to global trade led to a severe contraction in economic activity. In the first quarter of 2020, China’s economy shrank by 6.8%—its first contraction since the 1970s.

a) Supply Chain Disruptions:

China’s critical role in global supply chains meant that factory shutdowns in the country affected industries worldwide. Electronics, automotive, and textile manufacturing, among others, faced massive production halts due to a shortage of parts from China. While China managed to resume manufacturing faster than many other countries, the ripple effect of the supply chain disruptions lasted much longer, particularly as other economies went into lockdown.

b) Decline in Domestic Consumption:

Lockdowns and uncertainty about the future led to a sharp fall in consumer spending in China. While industrial production bounced back relatively quickly, the services sector, including retail, travel, and hospitality, suffered prolonged disruptions. Consumers became more cautious, reducing spending on non-essential goods and services, leading to a slower recovery in domestic demand.

c) Impact on Global Trade:

As the global economy contracted, demand for Chinese exports also declined. Major trading partners in Europe, the U.S., and other regions were grappling with the pandemic, and the global economic slowdown reduced demand for Chinese products. The slump in global trade further constrained China’s economic recovery.

d) Real Estate and Construction Slowdown:

China’s real estate sector, which had been a key driver of its pre-COVID growth, faced significant challenges during the pandemic. Home sales plummeted as people became uncertain about the future, and construction projects were delayed due to lockdowns and labor shortages. The resulting debt issues in the real estate sector, especially involving major developers like Evergrande, further strained the economy.

3. The Struggles of Post-COVID Recovery: What’s Ailing China’s Economy?

While many economies began to recover in 2021 and 2022 as vaccines were rolled out and restrictions eased, China’s recovery has been notably slower. Several factors have contributed to this sluggish rebound, raising concerns about the long-term health of the Chinese economy.

a) Zero-COVID Policy and Delayed Reopening:

One of the main reasons for China’s slow recovery was its strict Zero-COVID policy. Unlike most other countries that gradually opened up after the initial waves of COVID-19, China maintained stringent lockdowns and travel restrictions through much of 2021 and 2022. This policy disrupted both domestic activity and global supply chains, leading to prolonged economic stagnation. It wasn’t until late 2022 that China began easing these restrictions, delaying its recovery.

b) Real Estate Crisis:

China’s real estate sector remains in crisis. Major property developers, such as Evergrande, defaulted on massive debts, triggering fears of a financial contagion. The real estate sector is critical to China’s economy, accounting for up to 30% of GDP, directly and indirectly. With many construction projects stalled and home prices declining, consumer confidence has weakened, leading to reduced investments and spending in the sector.

c) Weak Domestic Consumption:

Despite the lifting of COVID-19 restrictions, domestic consumption has been slow to recover. The Chinese government has encouraged households to spend, but consumer confidence remains low due to economic uncertainty, rising unemployment, and fears of a prolonged slowdown. This lack of consumption growth is hindering the broader economic recovery.

While these stand as fresh issues for China, the other issues in the form of an ageing population, elevated debt levels, and a slowdown in global trade have only accentuated the dire straits.

4. Conclusion: The MSCI Index Shift and India’s Rising Star

The challenges facing China’s economy have been reflected in global market indices, such as the MSCI Emerging Markets Index. In recent years, China’s weight in the index has declined, while India’s has increased. Currently, in MSCI Global Index India’s weight is at 2.35 while China’s is at 2.34. This shift highlights the diverging fortunes of the two economies. If you wish to read about this in detail, we covered this topic in our previous newsletter edition.

a) Why India is Performing Better:

India’s economy, in contrast to China’s, has been growing steadily. Several factors explain India’s stronger performance:

- Demographic Advantage: India has a young and growing population, providing a large labour force and a growing consumer base.

- Policy Reforms: India has implemented economic reforms to attract foreign investment, such as easing regulations and improving infrastructure.

- Tech and Manufacturing Growth: India has become a major hub for technology and manufacturing, benefiting from companies seeking alternatives to China.

- Political Stability: India has seen relative political stability, which has provided a conducive environment for growth and investment.

b) China’s Struggles in Comparison:

China, on the other hand, is grappling with an ageing population, high debt levels, a struggling real estate sector, and the lingering effects of its Zero-COVID policy. These factors have made global investors more cautious about China, leading to a reduction in its weight in the MSCI Emerging Markets Index.

As global investors shift focus, the rise of India as a key player in emerging markets is evident, while China faces the long road to resolving its structural and cyclical economic issues.

Disclaimer: Investment in securities market are subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, membership of a SEBI recognized supervisory body (if any) and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The content in these posts/articles is for informational and educational purposes only and should not be construed as professional financial advice and nor to be construed as an offer to buy /sell or the solicitation of an offer to buy/sell any security or financial products.Users must make their own investment decisions based on their specific investment objective and financial position and using such independent advisors as they believe necessary.

Windmill Capital Team: Windmill Capital Private Limited is a SEBI registered research analyst (Regn. No. INH200007645) based in Bengaluru at No 51 Le Parc Richmonde, Richmond Road, Shanthala Nagar, Bangalore, Karnataka – 560025 creating Thematic & Quantamental curated stock/ETF portfolios. Data analysis is the heart and soul behind our portfolio construction & with 50+ offerings, we have something for everyone. CIN of the company is U74999KA2020PTC132398. For more information and disclosures, visit our disclosures page here.

You may want to read

India’s Great Ethanol Shift: What it Means for Your Portfolio

India’s Great Ethanol Shift: What it Means for Your Portfolio

Built for Every Market: How F.L.U.I.D Investing Navigates Market Moods

Built for Every Market: How F.L.U.I.D Investing Navigates Market Moods

Beyond the Balance Sheet: How Scuttlebutt Investing Works

Beyond the Balance Sheet: How Scuttlebutt Investing Works