The FPI Retreat: What’s Causing It?

India’s valuation & FPI’s

A strong 24% earnings growth in Nifty 50 stocks from FY21 to FY24, coupled with a surge in retail investor participation—through direct equities, SIPs in mutual funds, and insurance—had propelled the market valuation to remarkable highs. Between Sept 2023 – Sept 2024, the PE ratio of the Nifty 100 jumped up by 9.6%, Nifty Midcap 100 PE ratio surged by 79% to 45x and that of the Nifty Smallcap 100 was up 36.8% to 35.8x. We had highlighted the issue of frothy valuations in our Sept 24 AMA.

Since October 2024, Indian markets have been on a downward trend due to concerns over a weakening rupee, FPI outflows, rising oil prices driven by geopolitical tensions, and cautious investor sentiment amid high valuations. As a result, the Nifty Large, Mid, and Smallcap 100 indices have declined by approximately 12%-14%. This correction has also led to a drop in valuations, with the P/E ratio of Nifty 100, Nifty Midcap 100, and Nifty Smallcap 100 falling by 15%, 21%, and ~19%, respectively.

Foreign Portfolio Investors (FPIs) are entities that invest in a country’s financial assets, such as stocks and bonds, without seeking significant control over the companies. In India, FPIs play a crucial role in deepening capital markets by providing liquidity and fostering market efficiency.

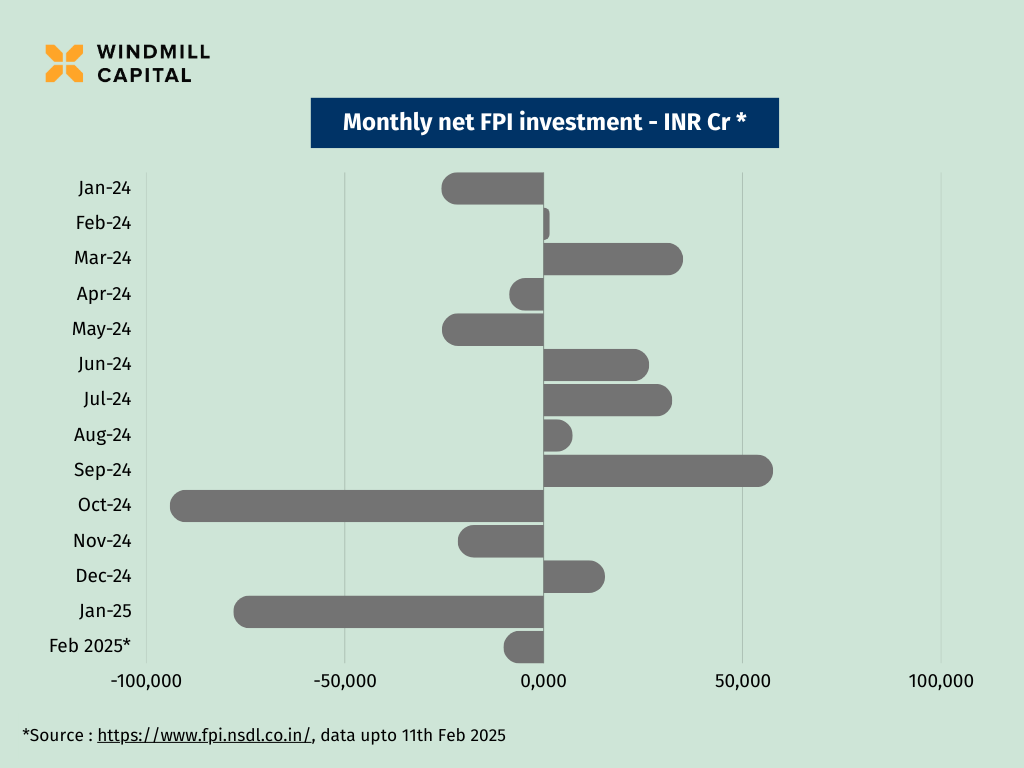

Foreign Portfolio Investors (FPIs) invested only ₹427 crore in Indian equity markets throughout 2024. However, in January 2025 alone, they withdrew a substantial ₹78,027 crore. This contrasts sharply with the approximately ₹1.7 lakh crore invested in 2023.

According to news reports, FII ownership in Indian equities has continued its downward trend, declining from 20.2% in January 2015 to 16.0% in January 2025, slightly below the 16.1% recorded in December 2024. As of January 2025, FII shareholding stood at 16.0%, reflecting a marginal sequential decline and remaining unchanged from October 2024, which marked a 12-year low. On a year-on-year (YoY) basis, FII ownership has fallen from 16.3% in January 2024, underscoring the persistent selling pressure.

Disappointing quarterly earnings and expectations of a subdued earnings season have made FPIs increasingly cautious. Additionally, uncertainty surrounding Donald Trump’s policies has prompted foreign investors to adopt a risk-averse stance, avoiding emerging markets perceived as volatile.

In January 2025, the rupee experienced a sharp depreciation, crossing the ₹87 per U.S. dollar threshold for the first time. By February 6, 2025, it reached a record low of 87.5825 against the U.S. dollar, influenced by growing bearish sentiment and a broader decline in Asian currencies. Significant FPI outflows have contributed to the rupee’s weakness, while a depreciating rupee, in turn, has deterred further foreign investments, creating a cyclical pattern of capital flight and currency depreciation.

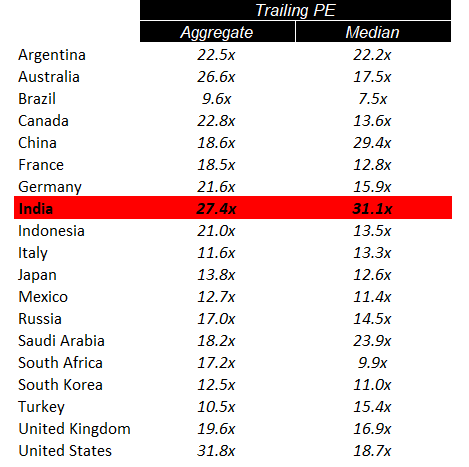

The elevated valuations of Indian equities have also contributed to the exodus of FPIs. Despite the recent correction, India’s valuation remains expensive compared to G20 countries, with an aggregate P/E ratio of 27.4x and a median P/E ratio of 31.1x—the highest among major economies except the U.S., which has an aggregate P/E of 31.8x.

Source: https://aswathdamodaran.blogspot.com/

Conclusion

While India’s markets experienced a strong earnings-driven rally, the surge in valuations—particularly in mid and small-cap stocks—led to concerns of overheating, which we previously highlighted. The recent market correction has brought some relief to valuations, yet India remains expensive relative to global peers, raising questions about the sustainability of further upside.

With weak consumption demand, sectoral challenges, and geopolitical uncertainties, investor sentiment remains cautious. While mutual funds continue to invest steadily, FPI inflows could remain tepid until valuations become more attractive or macroeconomic conditions improve. Moving forward, earnings growth will be a key determinant of whether the market stabilizes or faces further downside pressure.

Disclaimer: Investment in securities market are subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, membership of a SEBI recognized supervisory body (if any) and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The content in these posts/articles is for informational and educational purposes only and should not be construed as professional financial advice and nor to be construed as an offer to buy /sell or the solicitation of an offer to buy/sell any security or financial products.Users must make their own investment decisions based on their specific investment objective and financial position and using such independent advisors as they believe necessary.Windmill Capital Team: Windmill Capital Private Limited is a SEBI registered research analyst (Regn. No. INH200007645) based in Bengaluru at No 51 Le Parc Richmonde, Richmond Road, Shanthala Nagar, Bangalore, Karnataka – 560025 creating Thematic & Quantamental curated stock/ETF portfolios. Data analysis is the heart and soul behind our portfolio construction & with 50+ offerings, we have something for everyone. CIN of the company is U74999KA2020PTC132398. For more information and disclosures, visit our disclosures page here.

You may want to read