Portfolio Holding Analysis ft. Quality Smallcap – Smart Beta

Introduction & Performance

In this edition of smallcase in focus, we will deep dive into the analysis of the Quality Smallcap – Smart Beta (QSSB) smallcase. In our May edition, we presented a detailed analysis of the Value & Momentum smallcase which was highly appreciated by our readers. So we decided to replicate a similar analysis on Quality Smallcap – Smart Beta.

Let’s start off by looking at the key performance metrics of this smallcase since its launch, i.e. Dec ‘2020. Please bear in mind that the data set is between Dec ‘20 to July ‘24.

| Particulars | CAGR Returns | Risk-Adjusted Returns | Volatility | Max Drawdown |

|---|---|---|---|---|

| Quality Smallcap – Smart Beta | 42.2% | 2.0 | 21.1% | -22.6% |

| Equity Smallcap | 33.5% | 1.7 | 19.6% | -33.4% |

The table clearly indicates the superior performance of the smallcase, as during the specified period, the smallcase has delivered higher returns, and better risk-adjusted returns coupled with lower maximum drawdown.

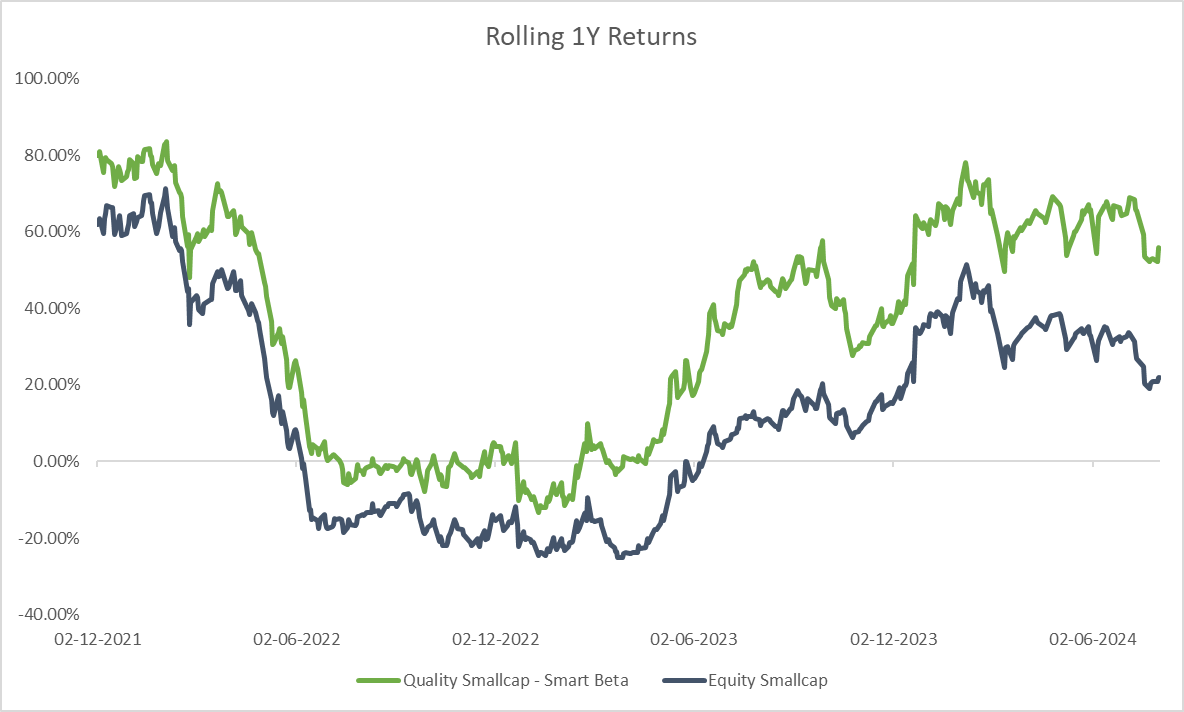

Rolling Returns

Let’s also take a look at the rolling 1-year returns of the smallcase and Equity Smallcap.

Point-to-point returns can be heavily influenced by short-term market fluctuations or unusual events that occur at the start or end of the measurement period. Rolling returns mitigate this by averaging out these effects over many periods. Rolling returns smooth out short-term volatility and provide a more consistent view of performance. This helps in understanding how an investment performs across different market cycles. The above chart clearly indicates that the QSSB has consistently performed better than Equity Smallcap.

Methodology

Now let’s talk about the methodology followed for stock selection when it comes to Quality Smallcap – Smart Beta. For you to understand the methodology behind this smallcase, first it is important to know about factor investing. You see, a factor is a broad and persistent driver of stock returns. There is a vast library of factors in the markets and each one of them has some contribution towards the returns of a stock. So which factors actually work? It depends on the asset manager’s research. The table provides a board list of factors that are usually accepted by all asset managers.

As the name suggests, for Quality Smallcap – Smart Beta one of the primary factors that we make use of is the Quality factor to drive stock selection for the smallcase. We use a proprietary Quality Score to shortlist stocks that exhibit the highest relevance with the quality factor. The Quality Score takes four major things into consideration –

a) Management Effectiveness or ROE

b) Financial Strength or Debt/Equity ratio

c) Earnings quality or Accrual ratio

d) Earnings performance consistency

Additionally, the smallcase only selects those quality smallcap companies whose price is experiencing a positive momentum trend. This improves the chances of the smallcase giving outsized returns. The smallcase attempts to shortlist at least 10 such stocks and will invest in Gold if the requisite numbers are not available. This nimbleness provides flexibility and enables efficient management.

Holding & Churn Analysis

Starting off with the basic analysis of the holding period stats. Take a look at the table below.

| Particulars | Hold Duration |

|---|---|

| Count | 91 |

| Min | 28 |

| Mean | 136 |

| Max | 545 |

This set of information is handy for us to make a base case understanding of the dynamics of the smallcase and how it has been managed over the years. For the uninitiated –

- Count – Refers to the total number of stock positions that have been a part of the smallcase (since inception).

- Mean – Refers to the average number of days a stock is held in this smallcase.

- Min/Max – Refers to the minimum/maximum number of days a stock was held in the smallcase.

The takeaway is in Quality Smallcap – Smart Beta, we have had 91 continuous positions across stocks with an average holding period of approximately 4.5 months (136 days) with maximum holding period for a stock going up to close to 1.5 years (545 days).

Moving on to the interesting bit around individual stocks returns. Let’s take a look at the scatter plots first.

The symbols that you see in the plots are abbreviations for stocks. For instance, ECLE is Eclerx Services, COCH is Cochin Shipyard, EXID is Exide Industries, and MAST is Mastek.

Now let’s discuss the few key inferences from the charts above –

- We have won big and lost small; in other words, we have carried on our winners and cut our losers. If you notice, our max gain on a winning stock has been ~214% while the max loss on a losing stock has been ~36%.

- The duration of holding on to the winners and losers is important too; ECLE or Eclerx Services, which has been the best performer, was held for ~300 days while the worst performer MAST or Mastek was held for less than half of it, close to 120 days.

- The interesting case of COCH or Cochin Shipyard is highlighted in black in both the scatter plots. Wondering why this stock is present in both the positive and negative plots? This is because we have held this stock in two different phases, one has given positive returns and one negative. The first phase where we held the stock was from Dec ‘22 to Feb ‘23 where the stock performed poorly and delivered negative returns. The second phase is from Mar ‘24 to the present where the stock has done phenomenally well.

This highlights a critical aspect of our smallcase management: we maintain objectivity and avoid bias toward any specific stock. We adhere strictly to our model strategy, avoiding unnecessary analyst discretion. Despite Cochin Shipyard’s initial underperformance, we reintegrated the stock whenever the model recommended, without any inherent bias, and achieved positive results. Our years of experience have taught us the importance of flexibility and eliminating all biases.

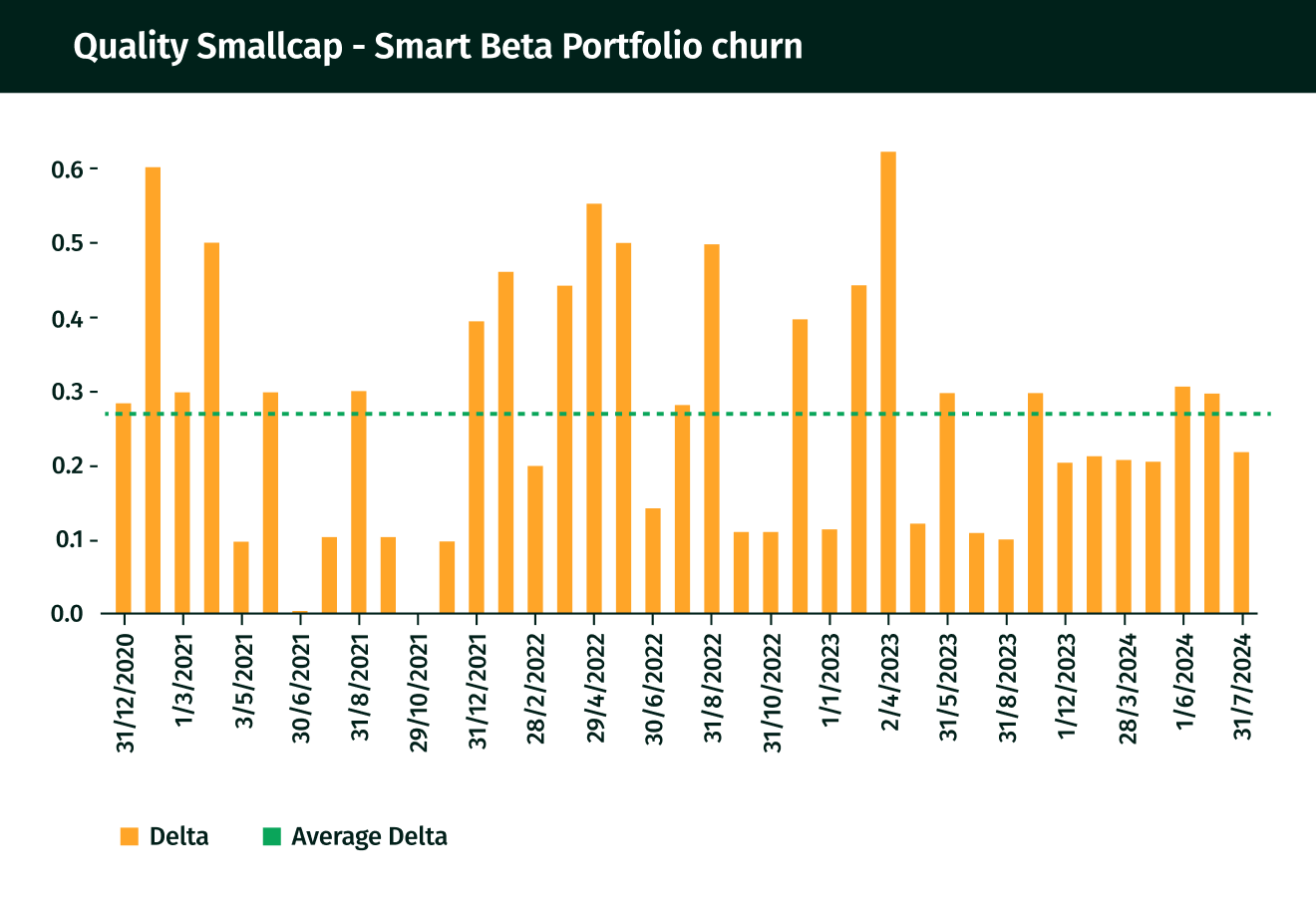

Lastly, let’s talk about the portfolio churn or turnover. Portfolio churn refers to the rate at which investments within a portfolio are bought and sold over a certain period. It measures the turnover of the assets and indicates how frequently the portfolio manager is buying/selling.

Given, it’s a monthly rebalanced smallcase, the portfolio churn is slightly on the higher side with an average churn of close to 30%. In simple words, on average in every rebalance 3 out of 10 stocks get churned, i.e. entered and exited. Moreover, Quality Smallcap – Smart Beta also has momentum as one of its factors, this also leads to higher churn as it’s a fast-changing indicator.

Evaluation of Portfolio Positions: Returns and Holding Period

Whatever is said and done, at the end of the day the key is to remain on the right side of things for the majority of the time and that is exactly what we have done with this smallcase. Out of the 91 stock positions we have taken in this smallcase, we have been on the right side 56 times and on the wrong side 33 times. However, the interesting aspect is that whenever we have been right, it’s been a big win and during times when we have been wrong, the loss is not drastic. You can gauge this with the average returns column, wherein for positive positions the average returns hover around 41% while for negative positions that number is -11%.

| Particulars | Count | % of Total Positions | Average Returns | Average Holding Days |

|---|---|---|---|---|

| Total Positions | 91 | 100 | 21.2 | 136 |

| Positive Positions | 56 | 61.5 | 40.9 | 166 |

| Negative Positions | 33 | 36.3 | -11.0 | 93 |

That’s all from this edition of smallcase in Focus. As always, the aim is to keep improving our processes for better results.

Disclaimer: Investment in securities market are subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, membership of BASL (in case of IAs) and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The content in these posts/articles is for informational and educational purposes only and should not be construed as professional financial advice and nor to be construed as an offer to buy /sell or the solicitation of an offer to buy/sell any security or financial products.Users must make their own investment decisions based on their specific investment objective and financial position and using such independent advisors as they believe necessary.

Windmill Capital Team: Windmill Capital Private Limited is a SEBI registered research analyst (Regn. No. INH200007645) based in Bengaluru at No 51 Le Parc Richmonde, Richmond Road, Shanthala Nagar, Bangalore, Karnataka – 560025 creating Thematic & Quantamental curated stock/ETF portfolios. Data analysis is the heart and soul behind our portfolio construction & with 50+ offerings, we have something for everyone. CIN of the company is U74999KA2020PTC132398. For more information and disclosures, visit our disclosures page here.

You may want to read