A 4-step Framework On How To Select The Right Portfolio 📝

Since the onset of COVID-19, the Indian markets have seen a surge in young, DIY investors. These investors enjoy researching and building their own investment portfolios, selecting stocks, mutual funds, smallcases, PMS options, and the like. While the thrill of crafting a personalized portfolio can be rewarding, focusing solely on isolated factors can lead to expensive mistakes. This narrow approach often results in disappointment and, even worse, can cause investors to abandon the market entirely.

In this guide, you’ll discover key mistakes to avoid and a proven 4-step framework for selecting portfolios like mutual funds and smallcases that align with your goals and risk tolerance. The results speak for themselves when investors make informed decisions based on a solid framework.

🔮 Past Performance Isn’t a Crystal Ball

One of the go-to ways for investors to choose a mutual fund, smallcase, or any other investment portfolio is sorting the funds by the highest returns, and picking the top 2-3 funds. You might be surprised, but simply choosing the top-performing funds based on past performance can be a recipe for disappointment. Let’s explore why this strategy is flawed.

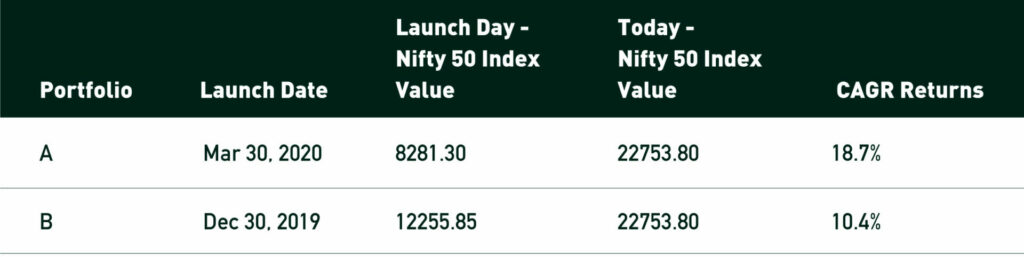

Why Base Period Matters 📊

One of the most common mistakes investors make is focusing on a portfolio’s past returns without considering the base period. The base period refers to the starting point for calculating returns. As the image illustrates two portfolios (A and B) launched at different times can have significantly different returns despite similar underlying strategies.

Imagine Portfolio A launched in March 2020 at the beginning of a market crash. On the other hand, Portfolio B started in December 2019, just before the crash. Naturally, Portfolio A will show higher returns simply because its base period was low in the market. This doesn’t necessarily mean Portfolio A is inherently better.

High Returns ≠ Low Risk 🚧

Many investors often use past returns as a proxy for risk assessment. But risk and return are typically positively correlated (read: risk and return are best friends). This relationship is often described as the risk-return tradeoff. While investments with higher historical returns may have outperformed the market or other investments in the past, investors need to assess the level of risk associated with those returns. High historical returns may be the result of taking on higher levels of risk, and there is no guarantee that those returns will continue in the future. Therefore, investors should consider both historical returns and risk factors when evaluating investment opportunities.

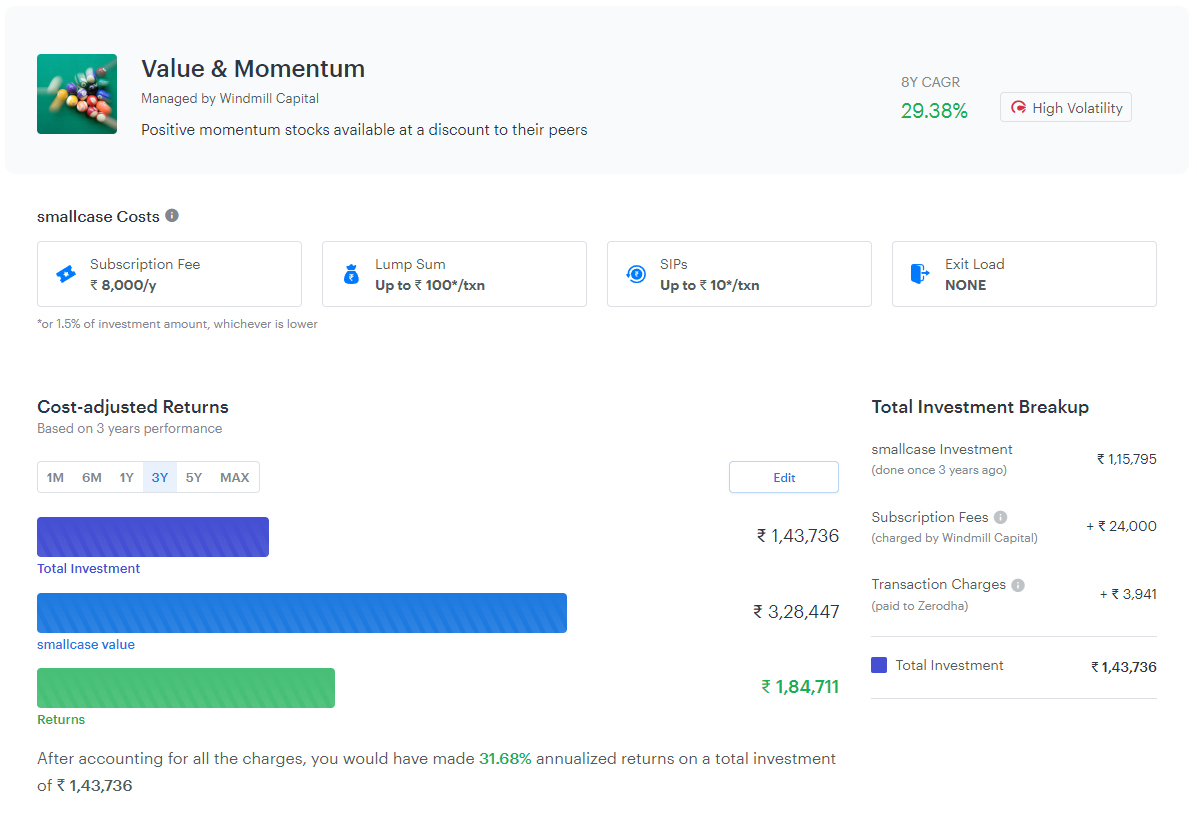

A classic example of such aforementioned behavior lies within our offerings. The Value & Momentum smallcase is popular because it has one of the highest CAGRs. However, it might not be suitable for risk-averse investors, as the smallcase mainly holds mid and small-cap stocks which are inherently riskier.

So, the chances of loss in our initial invested capital are higher and greater if the market suddenly tumbles based on any market-based news like the Iran-Israel war, the decision on US fed rates which is the opposite of what analysts were expecting, etc, which may have nothing to do directly with the companies in the Value & Momentum smallcase but affects the entire smallcase performance as the market as a whole goes in a panic or sell mode. And if everyone is selling, no matter how good the fundamentals are, your investment products/strategies/portfolios (mutual funds, smallcase, PMS, etc) are not going to be immune to this and as an investor, you will face the brunt. The differentiating factor will be the underlying product’s resilience to such market movements. As we all know, mid & small-caps react more on average to such negative movements in the markets than their large-cap counterparts, or equity as an asset class reacts more, as compared to asset classes like gold, bonds, etc, your investments in Value & momentum type of strategy is likely to be more severely affected. Hence the likelihood of loss in your investment capital is higher. This is what is essentially what we call risk. Equities as an asset class have greater risk than other asset classes and inside equities mid, small-caps tend to show greater risk than large-caps.

Tangled up in Biases? 🧶

Now, understanding this risk-reward relationship is crucial because it can easily get tangled up with emotional biases. For example, seeing an investment crush it in the past might make you want to jump in without considering the underlying risk profile. This is where the FOMO Frenzy kicks in.

The FOMO Frenzy: This focus on past returns can be fueled by the fear of missing out (FOMO), right? Seeing an investment crush it in the past might make you want to jump in without considering the underlying risk profile. But hold on! FOMO can lead to impulsive decisions and following the crowd, which could end up costing you.

Beware of Recency Bias: Here’s another mental trick your brain might play on you: recency bias. You might place too much emphasis on recent returns, neglecting the bigger picture of historical performance and long-term trends. Don’t get fooled by recent hot streaks!

Anchoring on Past Performance: Finally, be wary of anchoring bias. This is where you anchor your investment choices on past returns, using them as a benchmark for future expectations. But remember, past performance is no guarantee of future results. Anchoring on past returns can make you overlook other crucial factors and underestimate the uncertainty of investment outcomes.

🗒 Choosing the Right Portfolio: A 4-Step Framework

Here’s a practical 4-step framework to guide you to choose the right investment portfolio.

1. Understand Your Risk Profile 💡

This is the foundation of your investment journey. Consider these factors to assess your risk tolerance:

- Investment Goals: Are you saving for retirement (long-term) or a down payment on a house (shorter-term)?

- Time Horizon: How long can you stay invested before needing the money?

- Current Financial Situation: How much can you afford to invest without jeopardizing your financial stability?

- Emotional Response to Volatility: How comfortable are you with market ups and downs?

Your risk profile will determine the asset allocation (stocks, bonds, etc.) that’s right for you. A mismatch between your risk tolerance and your portfolio’s risk level can be costly.

2. Align Your Portfolio with Your Investment Theme 🤝

Consider the portfolio’s theme and ensure it aligns with your goals instead of investing in a portfolio because it has the highest returns. For instance, the theme of the Safe Haven smallcase is – ‘Low beta stocks that help protect against market volatility.’ We often receive queries from folks who have invested in this smallcase, enquiring why the smallcase returns are not in line with the overall market returns in recent times after the pandemic. This is because the smallcase tries to focus on low beta stocks which generally protect during the downside and perform more or less in line or sometimes underperforms during extreme bull markets. Hence the recent 3 years performance has not been in line with the overall markets. The rationale is that in the long run, markets go through phases of bull, bear, or sideways, and hence overall risk-adjusted returns should be better rather than only concentrating on the bull period.

3. Analyze Volatility and Risk-Adjusted Returns 🧮

Based on your risk profile, you should study the volatility and risk-adjusted returns of the portfolio. Volatility measures how much the price of a portfolio fluctuates. Risk-adjusted return measures how much return you get compared to the amount of risk you take. Let’s see how to use risk-adjusted returns while selecting a portfolio.

In the table, Portfolio C has a 3Y CAGR than Portfolio D, but its risk-adjusted return is higher. This suggests Portfolio C delivers better returns for each unit of risk taken, making it potentially more suitable for risk-averse investors.

To avoid base period bias of various investment products, you can also evaluate them on metrics such as rolling returns, max drawdown, beta, etc for a common period (do not compare 2 strategies/investments where one was launched 5 years back and one was launched 2 years back over their time-frame. The ideal would be to compare over a period which is <=2 years, in this example as the latest available performance for 2nd investment is only 2 years.)

4. Factor in Costs and Transparency 🔎

Before choosing a portfolio, understand the cost structure and level of transparency. Hidden fees can significantly eat into your returns.

Transparency: Look for clear information on fees, including:

- Management fees

- Transaction charges

- Exit loads (if applicable)

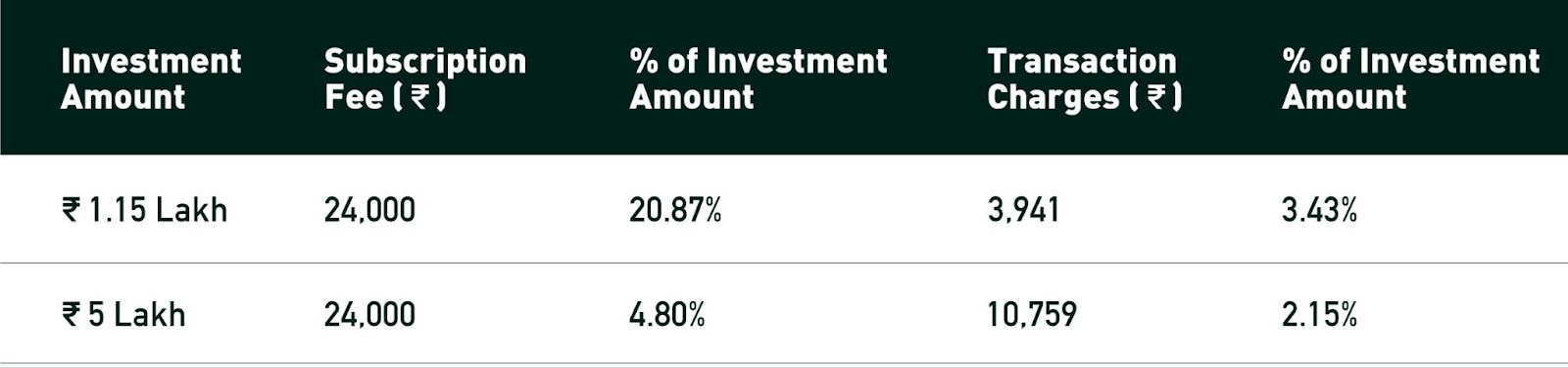

Cost Structure: For example, if you decide to invest ₹1.15 Lakh in the Value & Momentum smallcase, over the last 3 years these will be the charges associated with that investment, as shown below.

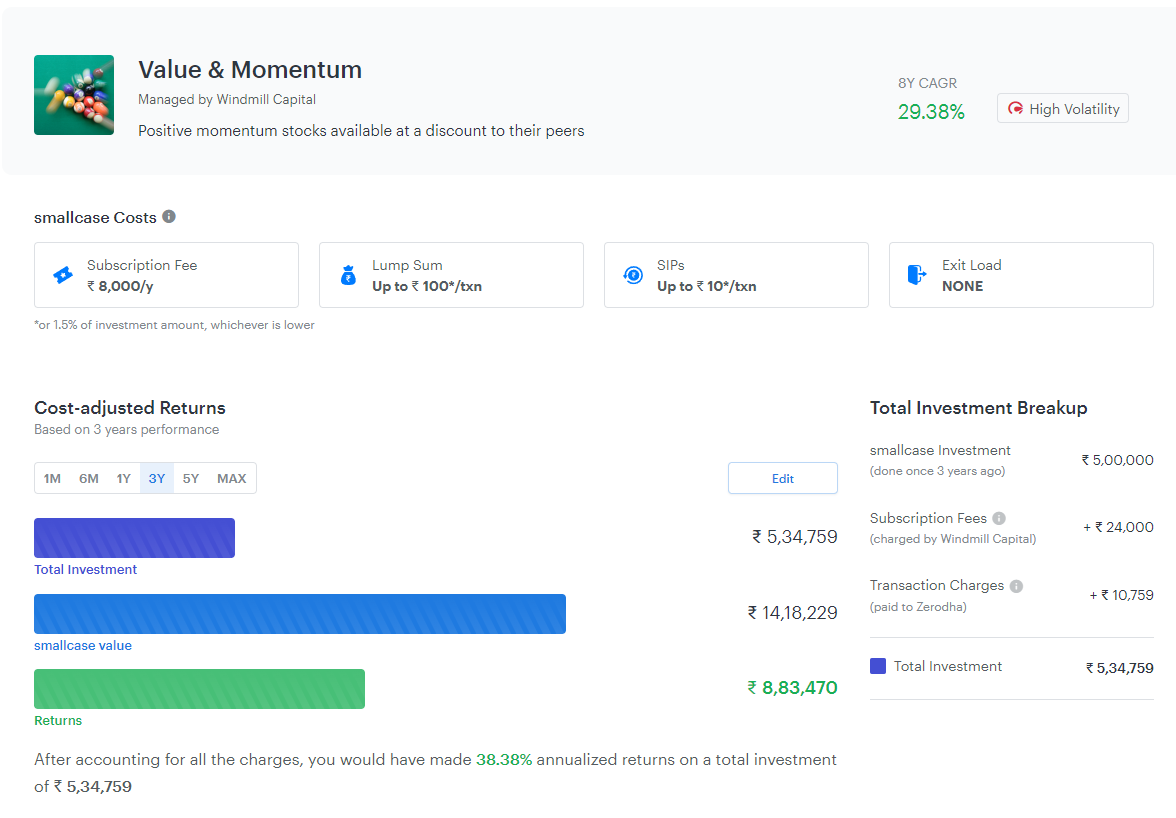

Now, if you increase the investment amount to ₹5 Lakh, things change drastically.

As a percentage of your investment amount, the charges drop substantially. The charges as a percentage of your investment amount become considerably low at higher investment amounts. On top of that, with a higher investment amount the returns you generate from the same portfolio also increase. This is in contrast to investment products which charge on an AUM basis. There the charges increase or decrease in line with your AUM and have no bearing on your initial investment amount.

Evaluating New Portfolios 🗃️

When evaluating a new investment portfolio, past returns are naturally unavailable. To make an informed decision, you need to shift your focus to other crucial aspects. Investigate the pedigree of the management team, potential risk factors, fees, and portfolio structuring, among others.

What About Underperformers? 😓

Don’t panic if a portfolio in your mix underperforms for a while. Instead, take a deep breath and assess the situation:

Analyze the Cause: What might be causing the underperformance? Is it a temporary market fluctuation or a more fundamental issue?

Consider Your Time Horizon: Investing is a marathon, not a sprint. If your goals are long-term (retirement, etc.), short-term dips may be less concerning.

Remember the example of our CANSLIM-esque smallcase. It underperformed in 2022 but rebounded strongly within a year. If you had a longer investment horizon and panic sold the smallcase in 2022 – it wouldn’t feel very nice, would it? It’s a different thing altogether if you wanted to redeem the smallcase in 2022 – you would most likely be better off shifting your investments to another smallcase.

✍️ Final Thoughts

At Windmill Capital, we’re passionate about empowering Indian retail investors. We believe transparency and clarity are paramount in building investment products that work for you. That’s why we created this 4-step framework – a roadmap to help you select a portfolio aligned with your risk tolerance and financial goals.

Until our financial paths cross again! ✌️

Disclaimer: Investment in securities market are subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, membership of BASL (in case of IAs) and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The content in these posts/articles is for informational and educational purposes only and should not be construed as professional financial advice and nor to be construed as an offer to buy /sell or the solicitation of an offer to buy/sell any security or financial products.Users must make their own investment decisions based on their specific investment objective and financial position and using such independent advisors as they believe necessary.

Windmill Capital Team: Windmill Capital Private Limited is a SEBI registered research analyst (Regn. No. INH200007645) based in Bengaluru at No 51 Le Parc Richmonde, Richmond Road, Shanthala Nagar, Bangalore, Karnataka – 560025 creating Thematic & Quantamental curated stock/ETF portfolios. Data analysis is the heart and soul behind our portfolio construction & with 50+ offerings, we have something for everyone. CIN of the company is U74999KA2020PTC132398. For more information and disclosures, visit our disclosures page here.

You may want to read