Banking Sector- Star Performer of the Markets

Let’s revisit Class 11 today. I’m sure all of us have read about the concept of Quantitative Tightening and Easing by the Central Bank, thanks to CBSE Class 11 Macroeconomics. Some of you might not even remember it but this is what we have been witnessing in the global economy for the last one year. Still confused? Do not worry, we are here for you.

I’ll start with the basics. You all know that during Covid 19, governments all around the world introduced stimulus packages (Quantitative Easing) to battle the negative growth rate and uncertainty that the world and global economy were witnessing. Every coin has two sides. This skyrocketed inflation. Here it is when central banks come up with a policy to cool down the heating economy, called Quantitative Tightening.

Now why do banks do this? The purpose behind this is to suck excess money out of the economy. There are many ways the banks can do it. But the most prominent one that has been happening is increasing interest rates. Banks increase interest rates which-

- Makes debt instruments like government bonds more attractive.

- Increases interest rates on loans that squeeze the demand for credit.

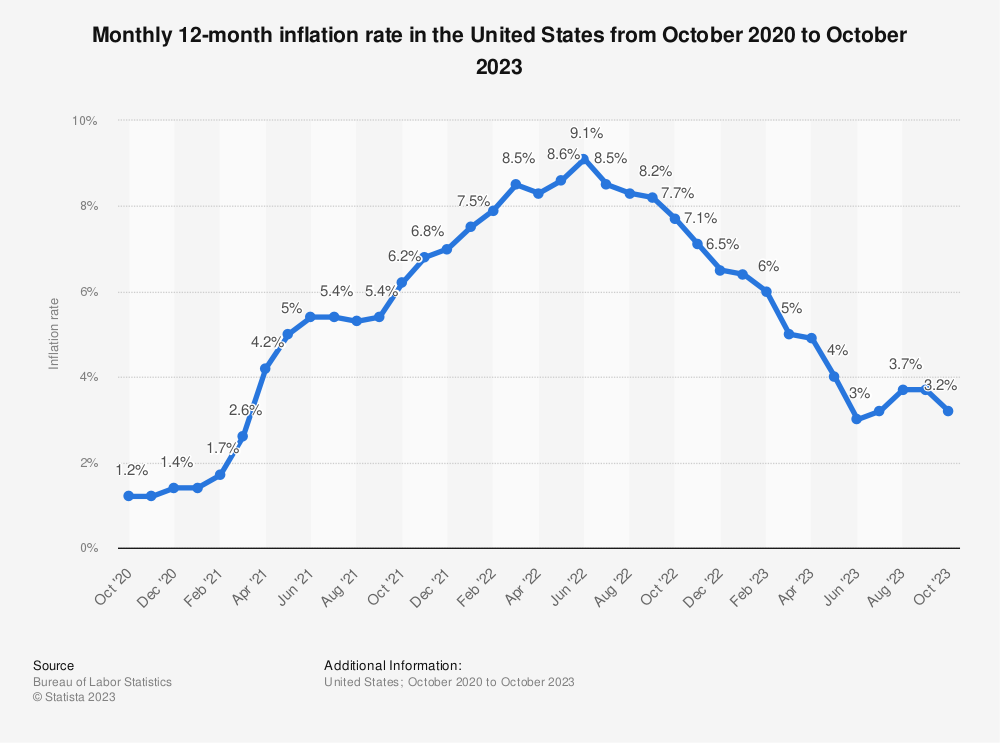

Dive into data:

Left- US inflation on an upward trajectory till it peaked at 9.1% in June 2022

Right- In a mere 14 months, the Fed increased the interest rates by 500 basis points, highest in the history

Source: Statista

We are done with the basics. Let’s move to the technical side of it. Think about this. If central banks increase interest rates, the repo rates (rates at which banks borrow from central banks) would increase and banks would ultimately pass it down to the consumer, increasing the loan rates right? Expensive Loans and high-interest paying deposits should discourage consumers from taking loans and decrease Net Interest Margins (Interest on Loans received- Interest on loans paid). But the story is different.

You’ll be surprised to know that NIMs have been on an upward trajectory since the interest rate hike cycle began, especially in India. Check the graph below.

Source- Telegraph India

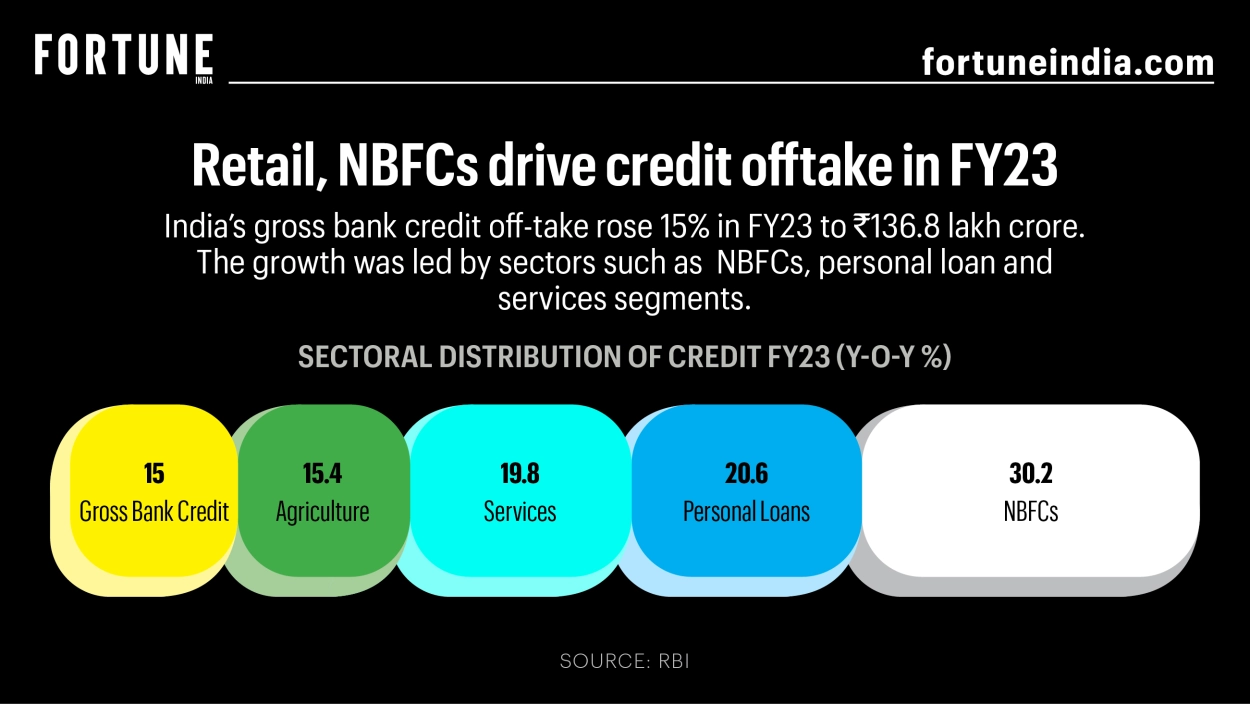

This is because of the Credit Offtake in India. Credit offtake, in simple terms, means the financing that banks provide to businesses and individuals. Look at the graphs given below. These clearly state that India’s credit offtake overpowered the effect of high-interest rates, thus the shining banking sector.

- India’s gross bank credit off-take rose 15% in FY23 to ₹136.8 lakh crore. The growth was led by sectors such as NBFCs, personal loans, and services segments.

- The increase in borrowing within a year has set the record of being the longest annual jump in credit offtake within the last eleven years.

- The most interesting thing is, that despite banks offering high deposit rates, India witnessed a slower deposit growth at 9.6 percent YoY compared to credit growth for the fortnight that ended on March 10, 2023.

Source- Fortune India

India’s growth and consumption story are amazing. It’s interesting to see how we as consumers are contributing to its growth. It’s not too long before India crosses Japan and Germany to become the world’s third-largest economy.

Well, I can go on and on about India and the growth that it has been witnessing but today let’s just keep it to the banking sector. Having said that, let us see what is up with the banking sector and where we, as a fund house see opportunity.

Disclaimer- All the facts mentioned below are stats-heavy.

Indian Banking Sector Outperforms US Counterparts as Q2 Results Surpass Forecasts

The second quarter results indicate that the Indian banking sector is relatively well-positioned compared to its US counterparts. Banks in India have reported stronger-than-expected earnings, with healthy profit growth of 33% year-on-year. In contrast, many large US banks have seen profits decline due to rising loan loss provisions and slowing growth.

Asset quality has also held stable for Indian lenders, with a steady drop in non-performing assets. However, in the US, delinquencies are beginning to rise across various loan segments like credit cards and auto loans, posing new risks. With stable credit costs and improving balance sheets, Indian banks appear better able to navigate the potential economic challenges that lie ahead compared to their US peers.

Analyzing Mounting Challenges for Smaller Deposit-Accepting Financial Organizations

The rising interest rate environment has exacerbated capital adequacy issues for some smaller Indian banks. Banks like RBL Bank and AU Small Finance Bank, which have capital adequacy ratios below the regulatory minimum of 15%, will need to raise billions of rupees to maintain credit growth without further weakening their capital buffers.

For those generating a quarter or more of revenues from credit cards, including RBL and Equitas SFB, funding expenses are expected to increase by 35-50 basis points as unsecured consumer loans sour. Without addressing thin capital cushions through equity infusions, these banks could see their loan portfolios constricted.

Change in Credit Risk Weight by RBI

RBI’s Move: Recently, the Reserve Bank of India (RBI) made changes to how banks and finance companies handle loans without collateral, like credit card loans.

- What Changed: The RBI increased the ‘risk weight’ for these loans by 25 percentage points to 125% from 100%. This means banks now have to set aside more money in case these loans aren’t repaid. For example, if a bank lends a loan of 100, 92 would be depositors’ money but 8 has to be shareholders’ capital if a loan is risky and unsecured, but after an increase in risk weight by 25%, the bank will have to give 10 from their side and rest 90 will be depositors money. This means they have to keep aside more % of the amount for riskier loans than they did before.

- Effects on Banks: This makes lending more expensive for banks. They might slightly increase the cost of loans in these categories, affecting borrowers.

- Impact on Profits: The change might affect bank profits slightly. Major banks like HDFC, ICICI, Axis, SBI, and Kotak could see around a 70-80 basis point change in their Common Equity Tier 1 ratios, which measure financial stability.

- For Finance Companies: Companies like Bajaj Finance, with more unsecured loans, might feel a greater impact. But given recent capital raises, this might not drastically alter their profits.

- Exclusions by RBI: The RBI’s warning doesn’t cover certain loans like home, vehicle, or education loans, loans against gold, or microfinance loans.

The Bottom Line: RBI’s move might make lending a bit pricier for certain loans, but it’s not expected to massively impact bank profits or significantly alter the financial landscape for finance companies in the long run.

Liked this story and want to continue receiving interesting content? Watchlist Green Portfolio’s smallcases to receive exclusive and curated stories!

Explore Green Portfolio smallcases

Green Portfolio is a SEBI Registered (SEBI Registration No. INH100008513) Research Analyst Firm. The research and reports express our opinions which we have based upon generally available public information, field research, inferences and deductions through are due diligence and analytical process. To the best our ability and belief, all information contained here is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable. We make no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results obtained from its use.

You may want to read

Indian Stock Market: The 2025 Lookback and the 2026 Watchlist

Indian Stock Market: The 2025 Lookback and the 2026 Watchlist

Four new innovative smallcases by Windmill Capital!

Four new innovative smallcases by Windmill Capital!

2024 in Review: Insights from Windmill Capital

2024 in Review: Insights from Windmill Capital

Green Portfolio

Green Portfolio